The Pradhan Mantri Mudra Yojana (PMMY) has officially completed 11 transformative years since its launch in 2015. As of April 2026, the scheme has evolved from a simple micro-credit facility into the backbone of India’s entrepreneurial ecosystem. Prime Minister Narendra Modi recently hailed the scheme’s progress, noting that it has successfully transitioned millions from “job seekers” to “job creators.”

11 Years of PM Mudra Yojana Performance Report: 2015 vs. 2026

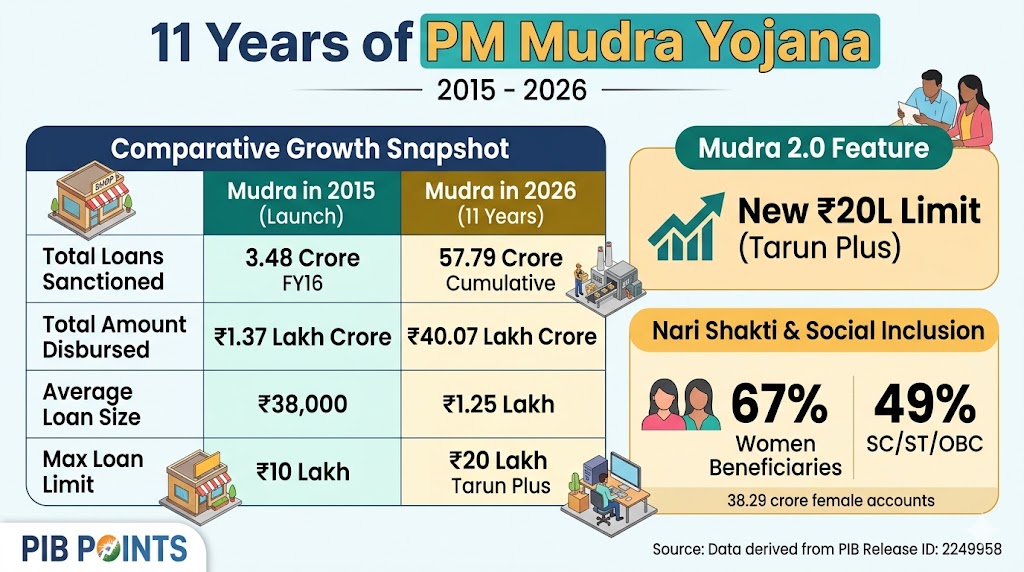

The growth of PMMY reflects a massive shift in India’s financial inclusion landscape. With the recent introduction of Mudra 2.0, the scheme now offers higher credit limits and simplified digital processing through the Udyamimitra Portal.

Comparative Growth Snapshot

| Parameter | Mudra in 2015 (Launch) | Mudra in 2026 (11 Years) |

| Total Loans Sanctioned | 3.48 Crore (FY16) | 57.79 Crore (Cumulative) |

| Total Amount Disbursed | ₹1.37 Lakh Crore | ₹40.07 Lakh Crore |

| Average Loan Size | ₹38,000 | ₹1.25 Lakh |

| Max Loan Limit | ₹10 Lakh | ₹20 Lakh (Tarun Plus) |

| Collateral Required | None | None (CGFMU Covered) |

The Evolution of Mudra Categories (Updated 2026)

The lending structure is designed to support a business at every stage of its lifecycle. The most significant update for 2026 is the Tarun Plus category, specifically for established units.

- Shishu: Loans up to ₹50,000 (Ideal for nano-enterprises and startups).

- Kishore: Loans from ₹50,001 to ₹5,00,000 (For purchasing equipment or initial expansion).

- Tarun: Loans from ₹5,00,001 to ₹10,00,000 (For established small businesses).

- Tarun Plus: Loans up to ₹20 Lakh (Available for units that have successfully repaid previous Tarun loans and wish to scale further).

Pro Tip: If you are looking to expand an existing business with higher capital, you should apply for PM Mudra Yojana Tarun Plus Loan to avail of the increased limit of ₹20 lakh.

Nari Shakti & Social Inclusion: The Core Success

The 11 Years of PM Mudra Yojana report highlights that the PMMY is not just an economic tool but a social equalizer:

- Empowering Women: Approximately 67% of total beneficiaries are women, with over 38.29 crore loan accounts belonging to female entrepreneurs.

- Inclusive Growth: Over 49% of loans have been disbursed to individuals in the SC, ST, and OBC categories, fulfilling the “Antyodaya” vision.

How to Apply for a Mudra Loan in 2026 (Step-by-Step)

To ensure your application is processed quickly and to avoid “Low Value” rejections, follow this checklist:

Required Documents Checklist:

- Identity & Address Proof: Aadhaar Card, PAN Card, or Voter ID.

- Business Proof: Udyam Registration, Trade License, or GST Registration.

- Financials: Last 6 months’ bank statement and a basic Business Plan (Project Report).

- Category Proof: SC/ST/OBC certificate (if applicable).

Application Channels:

- Digital: Apply via the Official Udyamimitra Portal.

- Physical: Visit any Commercial Bank, Regional Rural Bank (RRB), or NBFC.

Expert Insight: Why Some Mudra Loans Get Rejected

Based on current banking trends in 2026, here are the top reasons for rejection:

- Poor Credit Score: While collateral-free, a personal CIBIL score below 650 can hinder approval.

- Incomplete Business Plan: Banks need to see how the funds will generate income.

- KYC Mismatch: Ensure your Aadhaar name matches your business registration documents exactly.

Frequently Asked Questions (FAQ)

1. 1. How to apply for a Mudra Loan in 2026?

Eligible individuals can apply via the Udyamimitra Portal, directly at any Commercial Bank, RRB, MFI, or NBFC. You will need a simplified application form, identity proof, address proof, and a business proposal.

2. Is a guarantor required for the ₹20 Lakh Tarun Plus loan?

No. All Mudra loans are covered under the Credit Guarantee Fund for Micro Units (CGFMU) managed by the NCGTC, meaning no third-party guarantor or collateral is needed.

3. Can I apply for a second Mudra loan?

Yes. Once you repay a Shishu or Kishore loan, you can apply for a higher category (Tarun or Tarun Plus) to expand your business.

4. Is there any collateral required for a Mudra loan?

No, Mudra loans are collateral-free. They are covered under the Credit Guarantee Fund for Micro Units (CGFMU) provided by NCGTC.

5. What is the difference between Shishu, Kishore, and Tarun loans?

The difference lies in the stage of the business and the loan amount. Shishu is for beginners (up to ₹50k), Kishore is for mid-stage growth (up to ₹5L), and Tarun is for established businesses (up to ₹10L).

6. What is the interest rate for Mudra loans in 2026?

Interest rates are determined by individual banks (Canara Bank, SBI, HDFC, PNB, etc.) based on RBI guidelines. In 2026, rates typically range between 8.50% and 12% depending on the credit profile.

Source: Data derived from the Ministry of Finance and PIB Release ID: 2249958 (April 2026).

Comments are closed.